Our primary motivation was the regulation strategy imposed in the United States following the Savings & Loans crash of the 1980s. Regulators like William Black restricted growth of investment funds to 100%, and reportedly managed to pop the bubbles of several Ponzi schemes before they grew to substantial dimensions (mostly within their first one or two years).

A secondary motivation was to see if a Ponzi scheme operator imposing an internal limit on growth rate could prolong the life of the Ponzi scheme. This is based on the observation that Bernie Madoff apparently restricted entry into his particularly long-lived fund. In this project we model the growth and death of a stylized Ponzi scheme, defined for our purposes as a fraudulent investment system in which no generation of wealth takes place, so that principal and interest payments are financed out of the fund's total capital and hence depend on the growth rate of new investment in the fund. We then limit the growth of the Ponzi schemes to different rates to see how this regulation influences the scheme's persistence. We found that growth limits that weren't set low enough to collapse a scheme would prolong its existence.

We were also interested in how different learning rules and information networks on potential investors changed the regulatory strategy. We found that they had negligible effect. However, different investment strategies had an effect on the level of optimal growth limits.

We create a multi-agent model where investors can take on binary states (0 = not invested in the Ponzi scheme, 1 = invested in Ponzi). We assume that all agents invest in the Ponzi scheme when they learn about it from another agent. This assumption is based on standard finance theory, which claims that investors that are homogeneous with respect to risk aversion should generate equivalence of high risk / high return assets and low risk / low return assets due to arbitrage. With myopic investors, assets in fraudulent schemes should break out of this equivalence by seemingly yielding high returns at low risk (volatility). For example, Madoff reportedly paid out 10% interest with hardly any variance or correlation with the market. We ignore different classes of investors, such as secondary funds that channeled money to the Ponzi scheme

We create four iterations of the model with different parameters. Population size is fixed at 1000 potential investors, 10 of whom were initial investors. Each investor had $1 to invest and the Ponzi scheme promised a 10% return on investment every time step. Each iteration is run with no limits to growth and growth caps of 50%, 15% and 10%.

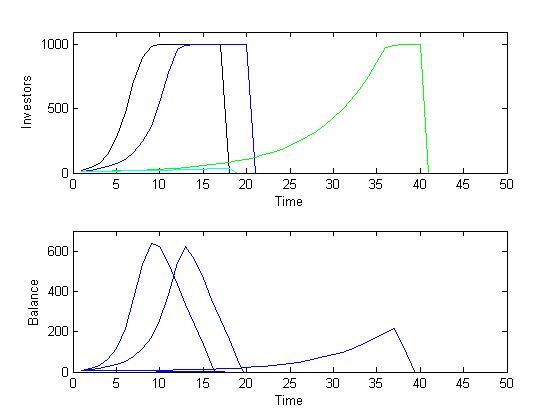

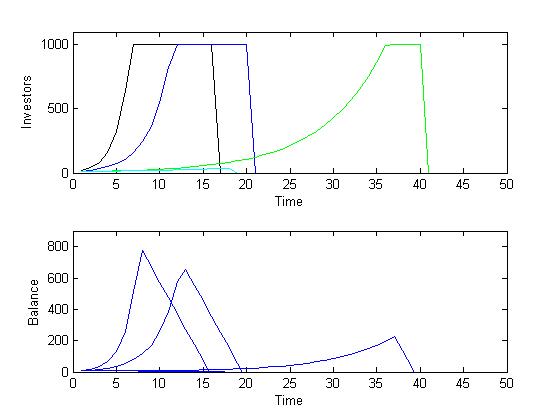

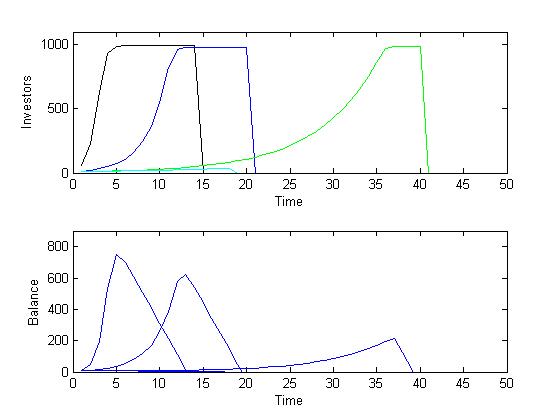

In the first three iterations, the fund is set up as distributing the promised 10% interest (which is treated as being consumed by investors). The disinvestment rate is set to zero in the first three iterations. These iterations differe in agents' learning rules regarding the Ponzi scheme. In the first iteration, individuals are randomly paired each time step; if one member of the pair is not an investor and the other member is, the former invests in the Ponzi scheme. In the second iteration, individuals are randomly paired six times each time step and if any agent's partner is an investor, that agent becomes an investor. In the third iteration, agents are connected by a random network with average connectivity (k) of four. If any of the agents' neighbors are investors, that agent becomes an investor.

The results of all three iterations are qualitatively similar and represented in Figures 1-3. Investment in the Ponzi scheme follows a traditional s-shaped diffusion curve, and eventually goes to fixation. As expected, higher connectivity leads to faster growth. Limiting the growth rate flattens the rate at which the Ponzi scheme spreads, and significantly prolongs the survival time of the Ponzi scheme but with little effect on the total capital bound up in the fund over its lifetime. However, when the cap on the growth rate equals the promised investment rate (here, 10%), then the scheme collapses early without a large number of investors or funds. This result is robust for different frequencies of pairings, different promised interest rates (not reproduced here) and different values of average network connectivity.

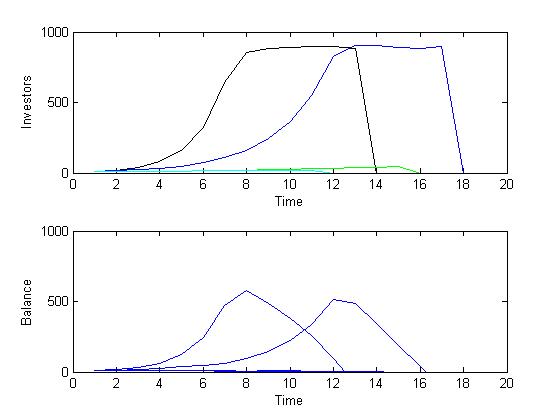

In the final iteration of our model, we explored the robustness of our results to a reinvesting fund scheme, in which promised interest is plowed back. In this case, the learning rules is identical to the network association in the third iteration. With a fixed probability of 10% every time step an agent chooses to disinvest in the scheme, withdrawing its principal and compound (imputed) interest. Agents may decide to reinvest, but only their initial $1 principal. Due to the effects of compound interest which increases the effective promised per-time-step return, we expect that the regulatory cap needs to be set at a somewhat higher level in order to collapse the scheme if the fund runs a reinvesting strategy, compared to a disbursing fund. The model confirms this expectations, as can be seen in the results in Figure 4.

Investment frauds are based on trust: Madoff was one of the most respected actors on financial markets. Including trust in the model might make the disinvestment schedule u-shaped, as distrust is high in the initial phase, falls as reputation spreads, and then rises as the fragility of the scheme becomes evident. Furthermore, in this case payouts will not only reduce the fund's total capital, but also increase confidence as neighbors observe the apparent stability and trustworthiness of the fund.

Heterogeneous agents with respect to risk aversion would allow to depart from standard finance theory, with a distribution in risk-return combinations between assets.

The salient feature of our model is the growth restriction, combined with the death of the system due to the disinvestment rate. One possible other application would be nuclear weapon agreements, in which countries voluntarily restrict the growth of their armament (and research), and in which the world could potentially become nuclear weapons-free if countries decided to pull out of nuclear armament. Another application would be vermin control, where only a limited amount of rodenticide is brought out for animal rights reasons, and birth control is applied instead.